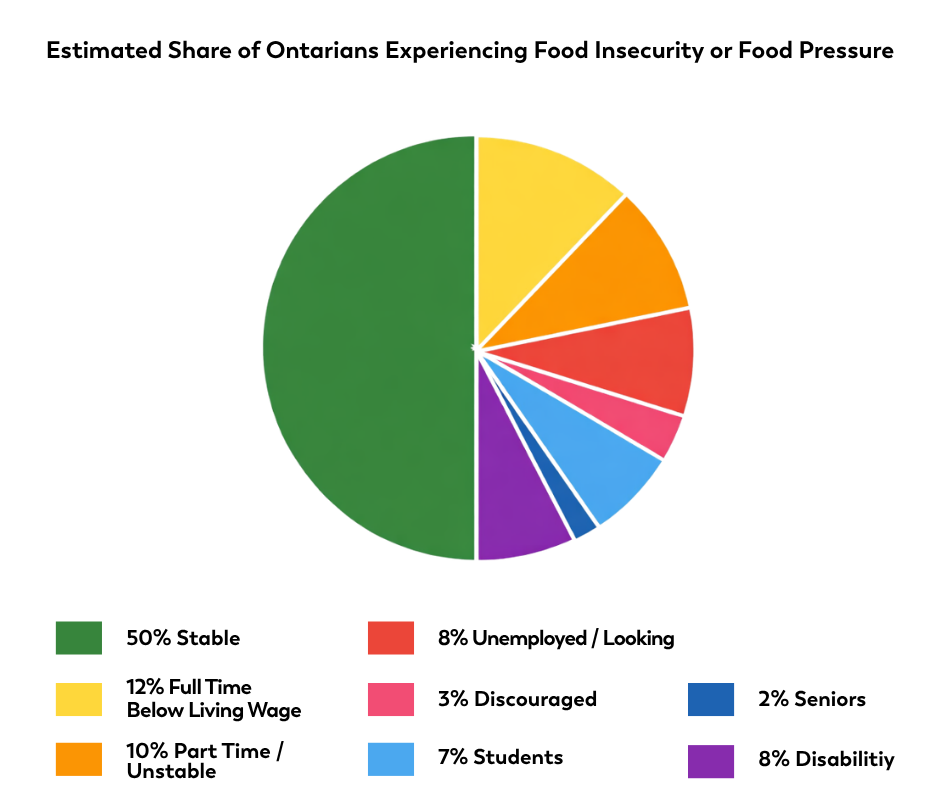

A few weeks ago, I wrote about a pie graph I had been building around poverty in Ontario.

The reason I started doing it was simple: I felt like we weren’t actually seeing the real numbers anymore.

So I started digging into the statistics myself.

How many people are on social assistance? How many are on EI? How many are working part time? How many are considered “working poor”? How many people are technically employed but still struggling to survive?

I wanted to understand the actual economic makeup of the province - not politically, not emotionally, but mathematically.

And before I even touched what we traditionally call the “middle class,” I had already landed at nearly 50% of the population living in poverty, near-poverty, or economically fragile conditions.

But after sitting with it longer, I realized I had left something major out of the equation:

The middle class.

And honestly, I shouldn’t have.

Because the more I thought about it, the more I started realizing that the middle class may actually be in deeper danger than many people officially categorized as “poor.”

Not because they necessarily make less money. But because they have more debt.

Massive debt.

Mortgages. Lines of credit. Car payments. Credit cards. HELOCs, (home equity line of credit). Consumer financing. “Affordable” monthly payments stretched over years.

For decades, credit created the illusion of stability. It allowed people to maintain a middle-class appearance long after real purchasing power began collapsing. And now the cracks are starting to show.

A recent federal report stated that nearly 50% of Canadians belong to the middle class. But that definition becomes increasingly disconnected from reality when you compare incomes against modern housing costs, food inflation, insurance, fuel, taxes, and debt servicing.

Statistics Canada data shows Ontario’s median household income sits around $91,000 before tax. On paper, that sounds solid. Years ago, that would have represented stability. Today, in many parts of Ontario, that income barely sustains a mortgage, groceries, utilities, transportation, childcare, and debt repayments.

Meanwhile, what’s considered “middle class” in Canada is often defined as households earning roughly between $57,000 and $115,000 annually.

But here’s the uncomfortable truth nobody wants to say out loud:

A household can technically be “middle class” while being one missed paycheck away from collapse.

That isn’t stability. That’s leveraged survival.

And we’re starting to see the cultural indicators everywhere.

Travel is one of the clearest examples because vacations are often the first thing families cut when economic pressure rises. Recent reporting shows Canadian travel demand continues to weaken significantly. Statistics Canada reported Canadian return trips from the U.S. fell again in early 2026, continuing a long downward trend. Other reporting found Canadian visits to U.S. metropolitan areas dropped as much as 42% year-over-year.

At the same time, surveys show many Canadians are avoiding travel altogether because they simply cannot justify the expense anymore.

That matters because the middle class has historically been the economic engine of discretionary spending.

When the middle class stops traveling, stops renovating, stops eating out, stops supporting local businesses, and starts pulling back in fear, the ripple effects move through the entire economy.

And I think that’s the stage we’re entering now.

What concerns me most is that many people still believe poverty looks like homelessness or visible desperation. But modern poverty often looks very different.

It looks like families carrying enormous debt while appearing “fine.” Two-income households unable to get ahead. People avoiding grocery stores because prices trigger anxiety. Parents quietly skipping meals. Adults with decent jobs unable to buy homes. Households financing basic necessities. People one interest-rate increase away from disaster.

In many ways, the middle class became the buffer zone holding the entire economic structure together. And if that buffer collapses, society changes very quickly — not just economically, but socially, psychologically, and politically.

Because once people realize they followed all the rules and still can’t build security, trust in the system starts to erode.

That’s why I keep coming back to local systems. Local food. Local production. Local relationships. Local resilience.

Because the larger the systems become, the more fragile ordinary people become inside them.

And maybe that’s the real story unfolding beneath the headlines right now: not simply that poverty is growing, but that the line between “middle class” and “poverty” is disappearing altogether.

Locally yours,

Small Scale Farms

|